LO&G members have extensive experience to carry out economic evaluations for asset deals.

In case of share deals (i.e. acquisition of a company), additional support from investment bankers and / or accounting companies should be seeked due to the complexity of the subject and the necessity to also evaluate impacts of accounting and balance sheets

LO&G economic evaluation includes

- Analysis of respective Licensing / Contracting agreement and set up of corresponding economic model on Excel basis

- Set-up of Life of Field sheet (i.e. technical input) and commercial input (i.e. Price scenarios, inflation, etc.)

- Cash flow analysis with all relevant parameters

- Internal Rate of Return (IRR), internal rentability of a cash flow, defined as discount rate which results in a zero NPV. If IRR of a project is higher than the company’s internal discount rate, the project is attractive.

- Net Present Value (NPV, discounted cash flow) at different discount rates. If NPV at company’s internal discount rate is positive, the project is attractive.

- Pay Out Time, i.e. time to reach a no profit no loss situation (undiscounted) or a given rentability (discounted)

- Break Even Price Analysis, i.e. hydrocarbon price needed to achieve a no profit no loss situation (undiscounted) or to achieve a given rentability (discounted)

- Others, if needed

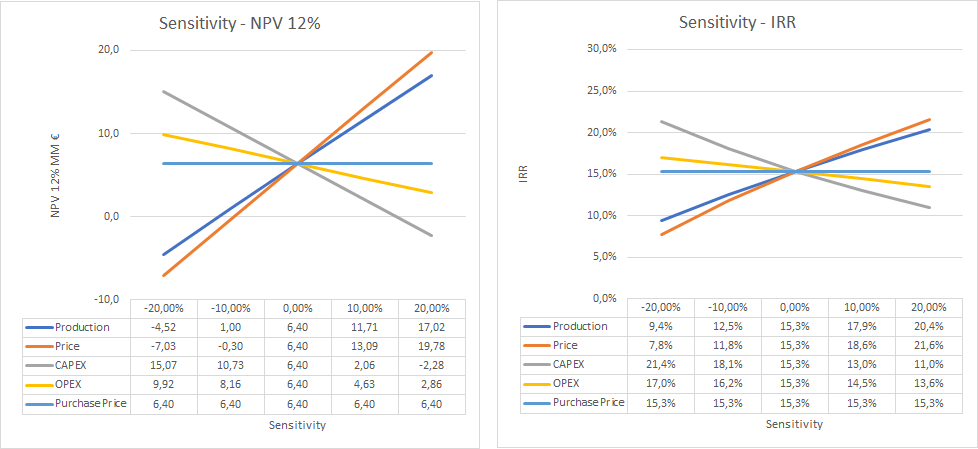

- Sensitive Analysis (Ceteris Paribus)

Economic Results (NPV based or IRR based) are shown for changes of one single input parameter (e.g. Production, price, capex, etc.). All other input parameter are unchanged

This analysis shows the impact of one single input parameter on the overall economic results

- Scenario Analysis

If applicable, different scenarios (i.e. change of more than one input parameter) can be analysed.

If contractual terms are still negotiable (i.e. Government Take and / or Farm-In/Out or acquisition conditions), scenario analysis may be extended to contract terms

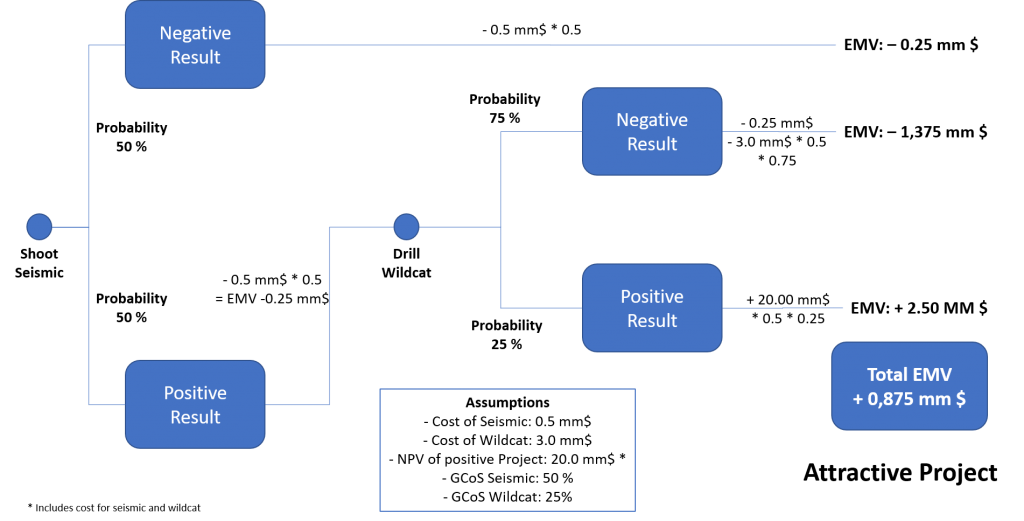

- Risk Analysis – EMV Calculation

Especially exploration projects are under high uncertainty. To make appropriate decisions under uncertainty, calculations of the Expected Monetary Value (EMV) are used.

The EMV is defined as the difference between the the Net Present Value of the Project multiplied with an estimated Chance of Success (CoS) minus the NPV of the risk capital multiplied with (1 – CoS). Often more than one decision level are relevant by using a decision tree matrix. If the calculated EMV is positive, the project is attractive.

Example for two decision level: